Essential Forms

Easily manage key IRS forms like Form W-9, Form W-8BEN, Form 8655, FinCEN BOIR and more.

Tools & Calculators

Quickly calaculate taxes and find deadline with our trusted tools.

Form 2290 Tax Calculator

Estimate your HVUT quickly

990 EIN Finder

Locate and verify nonprofit EINs with ease for IRS Form 990

Form 7004 Due Date Calculator

Find the exact extension deadline

Contact & Support

Reach out for personalized help

Resources & Articles

In-depth form breakdowns

Guides & How -To-Articles

Knowledge Center

Walkthroughs, expert Q&As and Tutorials

Compare Alternatives

TaxZerone vs Tax1099

Knowledge Base

Step-by-Step guide and FAQs

Blog & Trending Topics

Tax tips, industry changes and updated

Learning Hub

YouTube Videos

Walkthroughs, expert Q&As and Tutorials

Attention Nonprofits! E-file your 2025 Form 990-N today to maintain your tax-exempt status and IRS compliance.

IRS-Authorized

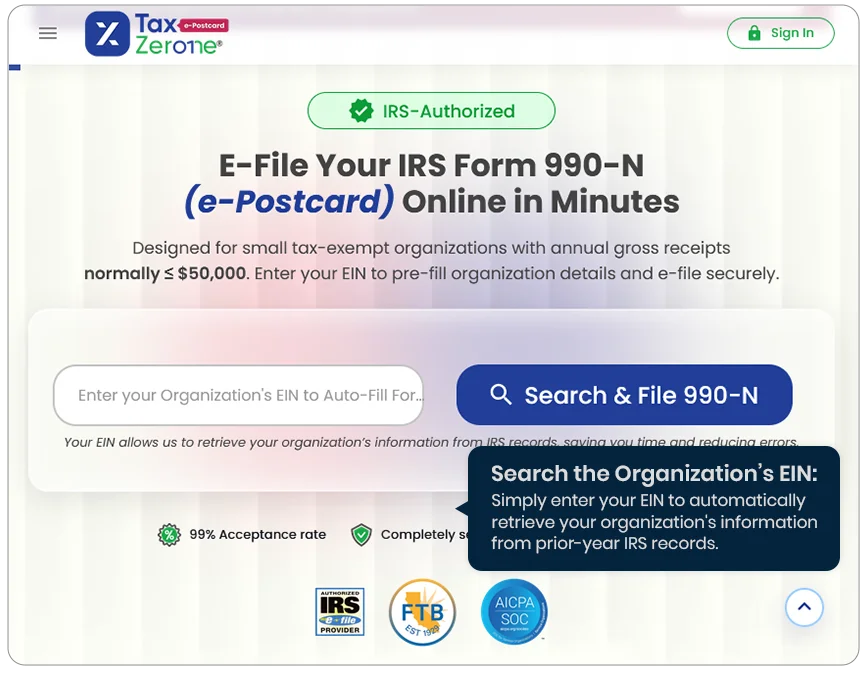

E-File Your IRS Form 990-N

(e-Postcard) Online in Minutes

Designed for small tax-exempt organizations with annual gross receipts

normally ≤ $50,000. Enter your EIN to pre-fill organization details and e-file securely.

Your EIN allows us to retrieve your organization’s information from IRS records, saving you time and reducing errors.

99% Acceptance rate

Completely secure

Receive instant update

File Form 990-N online

Choose TaxZerone for a simple, secure, and reliable

Form 990-N filing experience.

How to File Form 990-N (e-postcard)?

Follow these 3 Simple Steps Designed for Eligible Tax-Exempt Organizations.

Step 1: Search by EIN

Enter your EIN to automatically retrieve your organization's information from IRS records.

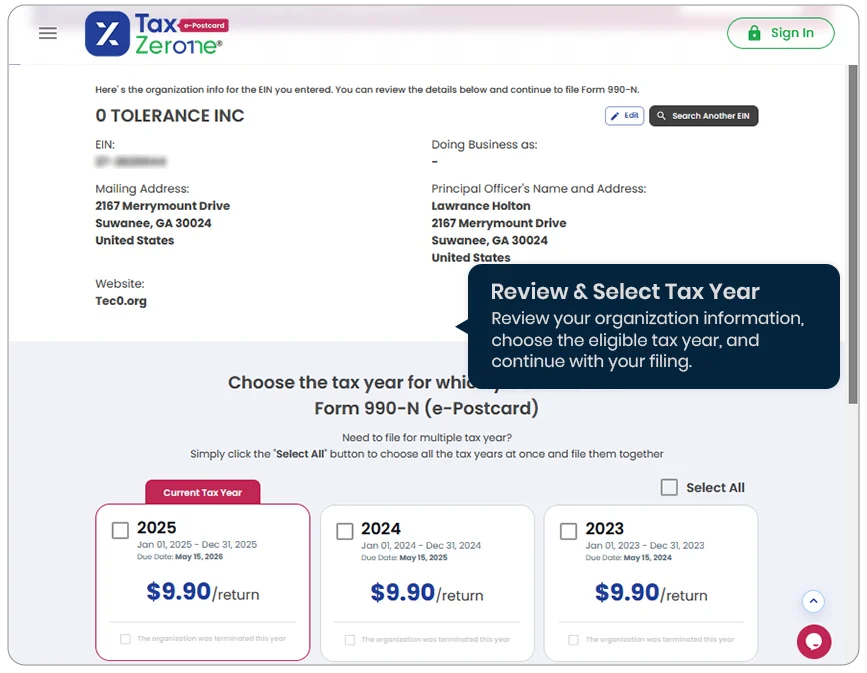

Step 2: Review & Choose Tax-Year

Review your organization's details and select the applicable tax year.

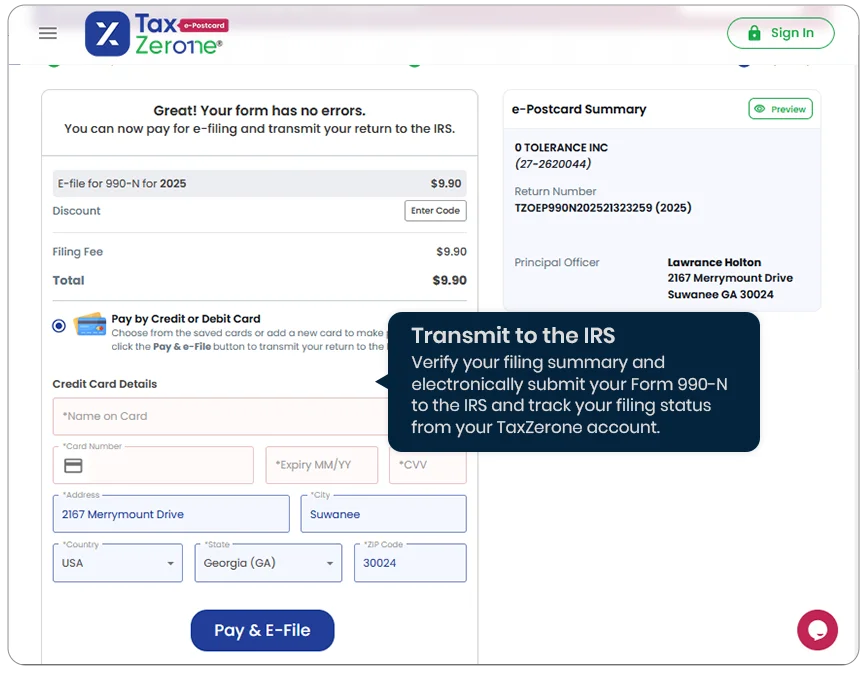

Step 3: Stay Exempt

Now securely transmit your Form 990-N (e-Postcard) information to the IRS.

What is Form 990-N (e-Postcard)?

If your nonprofit is small, Form 990-N might be all you need. Here’s what it means for you:

- Gross Receipts Threshold: Organizations with annual gross receipts of $50,000 or less are eligible to file Form 990-N instead of Form 990 or Form 990-EZ.

- Electronic Filing Only: Form 990-N must be submitted online. It cannot be filed on paper

- Simplified Annual Notice: This is the shortest and simplest IRS filing option for small tax-exempt organizations.

- Annual Filing Requirement: The form must be filed every year to maintain tax-exempt status.

- Automatic Revocation Rule: If an organization fails to file for three consecutive years, the IRS will automatically revoke its tax-exempt status.

If your organization qualifies under the $50,000 threshold, Form 990-N is the easiest way to stay compliant with IRS annual reporting requirements.

Who Must File IRS Form 990-N?

Wondering if Form 990-N (e-Postcard) is right for your organization? Here’s a simple way to know:

- Small Nonprofits: Organizations with annual gross receipts of $50,000 or less must file Form 990-N.

- Basic Information Only: The filing is simple and only asks for:

- Organization’s legal name

- Employer Identification Number (EIN)

- Mailing address

- Website (if applicable)

- Confirmation that gross receipts are within the $50,000 limit

Form 990-N is a quick online filing that helps small nonprofits stay compliant without the complexity of a full tax return.

Why Choose TaxZerone?

Check out the features that make TaxZerone an ideal choice for exempt organizations to e-file 990-N returns.

IRS Authorized

File your Form 990-N accurately with TaxZerone, an IRS-authorized e-file service provider, and be assured that the return is accepted by the IRS.

Free EIN Finder

TaxZerone's EIN Finder let you enter a non-profit's name or EIN and quickly see the information pulled from its past IRS filings.

Free Retransmission

Free Retransmission In case the IRS rejects Form 990-N due to any errors, you can correct the mistakes and retransmit the return without any additional fee.

Pay Securely with PayPal

Complete your filing securely using PayPal which will make the process faster, and easier.

Complete Filing in Few Minutes

TaxZerone helps you complete your filing in just a few minutes with a quick and simple process. When the IRS updates your status, we instantly notify you via email within minutes - keeping you informed until your filing is fully processed.

Friendly Support

Our dedicated friendly support team will help you with any queries or filing issues via email, chat and phone (English & Spanish).

TaxZerone provides filing support for the 2025 tax year and prior years, including 2024 and 2023,

helping your organization maintain compliance efficiently.

E-file Form 990-N

(e-Postcard) on the go!

Download our mobile app (available on iOS and Android), e-file your Form 990-N, and stay exempt.

Ready to try? Install the app now!

Hear What Our Users Say About Us

- Jennifer Burton

- Tamara Fowler

- Poul Chad Larsen

Frequently Asked Questions

1. How to file Form 990-N (e-Postcard)?

Form 990-N (e-Postcard) can only be filed electronically. With TaxZerone, you can complete the filing in 3 simple steps:

- Enter your EIN to retrieve your organization's information stored in the IRS database.

- Review whether the information is correct and make changes if necessary.

- Choose the tax year and transmit your Form 990-N (e-Postcard) to the IRS.

2. When is the due date to file Form 990-N?

Form 990-N must be filed by the 15th day of the 5th month after the close of the tax year. For example, if your organization's tax year ended on November 30, 2025, the Form 990-N deadline is April 15, 2026.

3. Who can file Form 990-N (e-Postcard)?

4. What information is required to file Form 990-N?

The following information is required to file Form 990-N (e-Postcard) with the IRS:

- Organization’s Employer Identification Number (EIN)

- Tax year (calendar or fiscal)

- Legal name and mailing address

- Any other names the organization uses

- Name and address of a principal officer

- Website address (if available)

- Confirmation that the organization’s annual gross receipts are $50,000 or less

- If applicable, a statement that the organization has terminated or is terminating

5. What happens if I don't file Form 990-N?

Related Resources

Form 990-N Instructions

Read the Instructions for Form 990-N to file accurately with TaxZerone

Form 990-N Due Date

Know more about the Due Date of Form 990-N and file your form on time.

Form 990-N EIN Finder

Try out Form 990-N EIN Finder to fetch your organization's information.

About TaxZerone®

TaxZerone® is an IRS-authorized e-file service provider that helps businesses, individuals, and nonprofit organizations file multiple IRS forms, such as business tax, excise tax, employment tax, extension, information returns, and tax-exempt forms, easily and securely.

Terms of Use | Privacy Policy | Cookie Policy